I’m sure by now that most readers will be aware that this week National Savings & Investments closed for sale its RPI+1% index linked savings certificates (ILSC’s). If they stay closed for a long time or even reopen in a few months linked to the CPI instead of RPI its going to give me and I’m assuming many others a few problems. My retirement investing strategy uses NS&I ILSC’s extensively. I currently have 20.7% of my net worth ties up in them.

Sunday 25 July 2010

Wednesday 21 July 2010

Positive real savings rates are impossible to find - Average UK savings interest rates – July 2010 Update

Tuesday 20 July 2010

The Real Pay Cuts Begin – Average UK Earnings – July 2010 Update

Monday 19 July 2010

It will always be inflation – UK Inflation – May 2010 Update

Sunday 18 July 2010

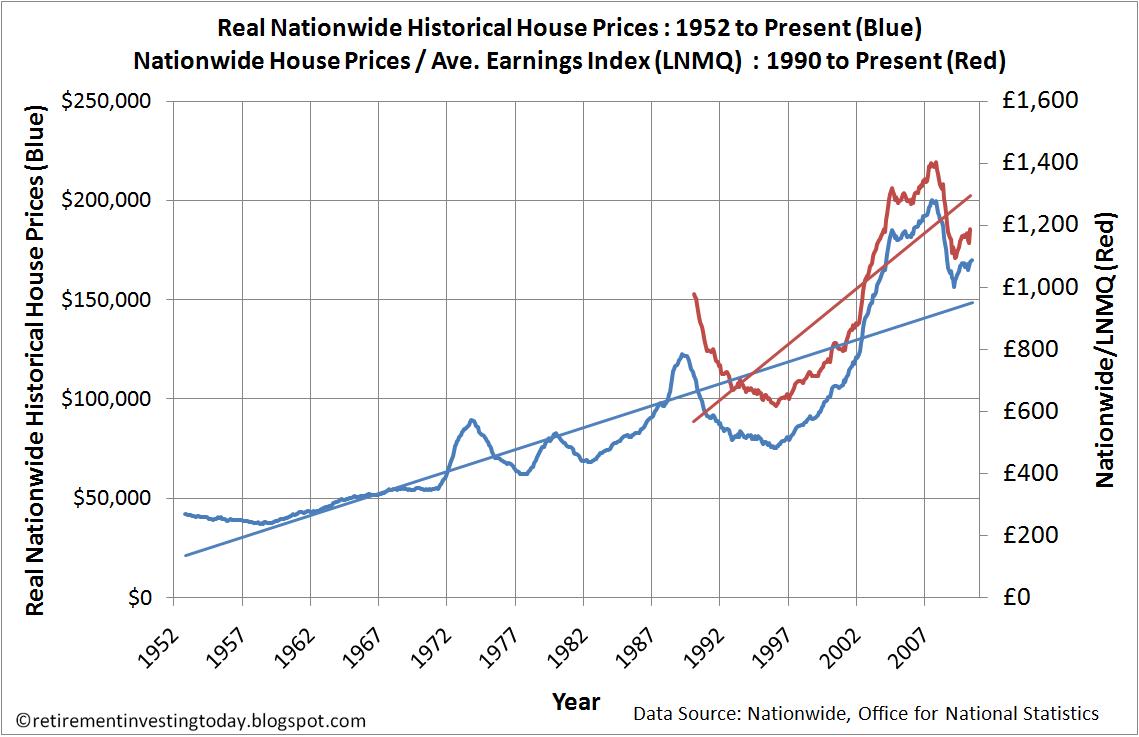

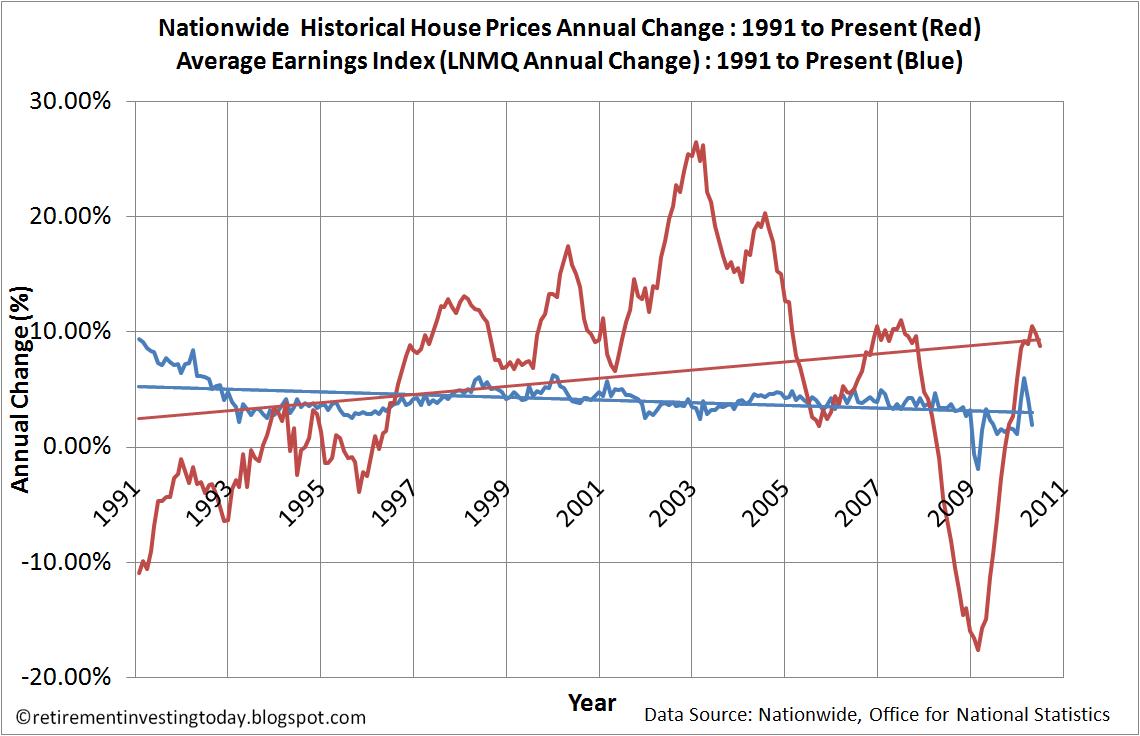

Houses are still overvalued - UK property market – July 2010 Update

Subscribe to:

Posts (Atom)